|

Region |

5-Year Price Growth (2020–2025) |

Q2 2025 QoQ Growth |

Average $PSF (Q2 2025) |

|---|---|---|---|

|

CCR |

19% |

+3% |

$2,850 |

|

RCR |

35% |

+1.2% |

$2,350 |

|

OCR |

40% |

+0.5% |

$1,950 |

Is CCR Bouncing Back?

For years, Singapore’s Core Central Region (CCR) lagged behind the suburbs. Investors poured into RCR and OCR while CCR looked… sleepy.

But something just changed.

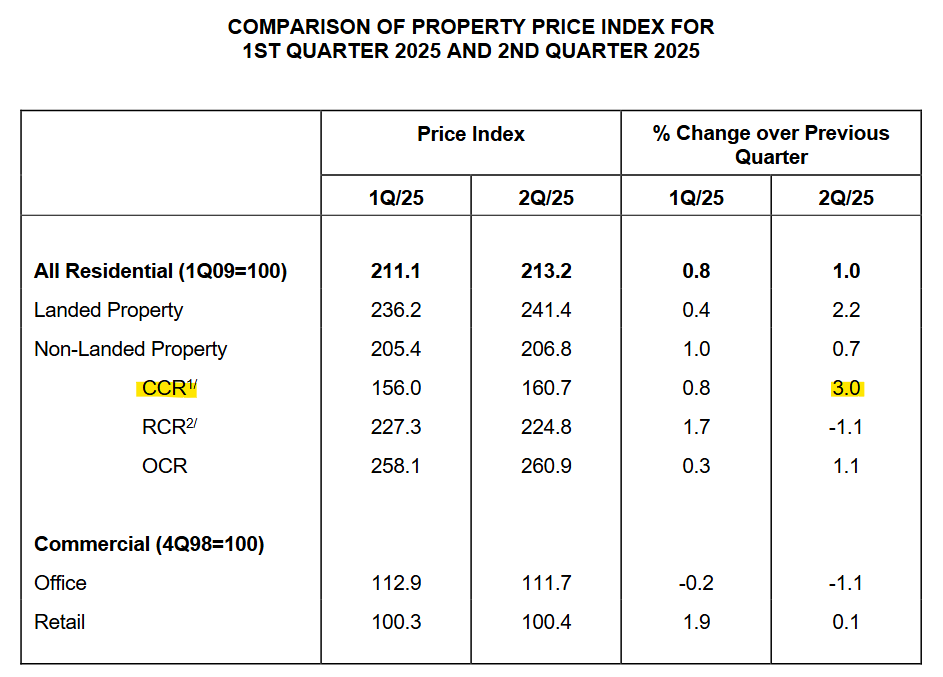

According to URA, CCR pulled ahead with a 3.0% QoQ price jump in Q2 2025 — the strongest among all regions — while RCR slipped and OCR stayed moderate.

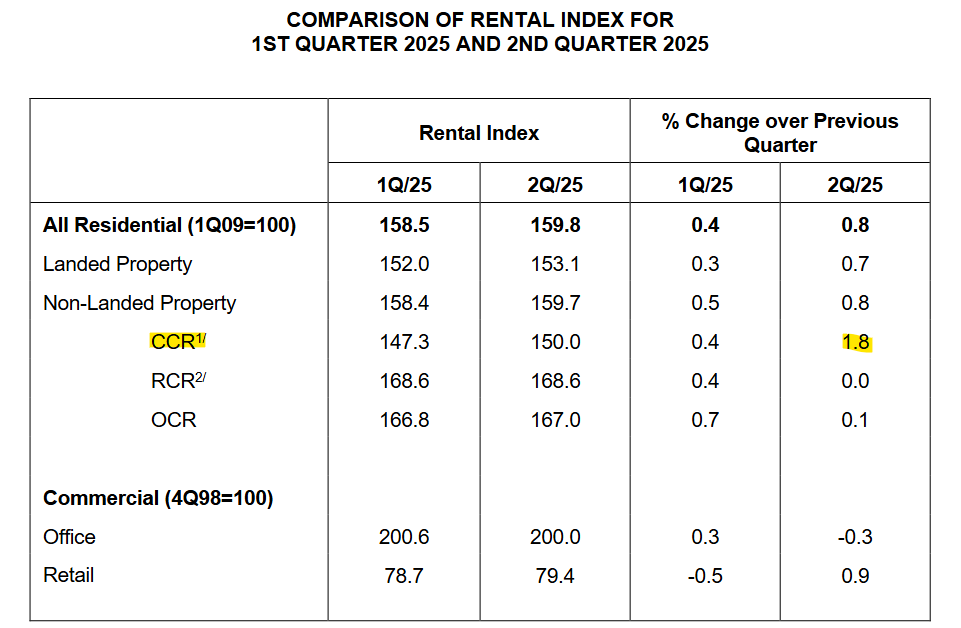

Private rentals grew 0.8% QoQ, but CCR stood out with 1.8% growth, showing demand isn’t just talk—it’s transaction-based.

Is this the long-awaited turning point for prime property? Or just a blip before the next cooling measure bites?

In this article, I’ll break down what the numbers really mean. If you’ve ever thought about owning in Singapore’s golden core, this could be the moment to pay attention, before everyone else realises it.

This 3.0% Jump Is a Rare Opportunity

The Core Central Region isn’t just another district — it’s Orchard, River Valley, Tanglin. It’s where global buyers plant their flag when they want the best of Singapore.

Since the COVID low, the numbers show CCR climbed only about 24%, while the RCR and OCR sprinted ahead by nearly 50%. Many investors dismissed the core, chasing faster gains in the suburbs.

But property markets move in cycles and the core never stays discounted for long. This 3.0% is the clearest signal in years that the tide is turning back toward the city’s most prestigious addresses. If you’ve been waiting for the moment when the CCR starts to lead again — you’re looking at it.

Numbers Don’t Lie: CCR’s Catch-Up Potential

Let’s look at the numbers together. As of Q2 2025 (URA data):

CCR is the only region that’s underperformed in the last five years… and yet it’s the only one showing real momentum right now. That combination doesn’t come around often.

So, what does this really mean for you?

- If you’re global → CCR isn’t just Orchard or River Valley on a map. It’s Singapore’s “front-row seat.” Compared to Hong Kong, London, or New York, our luxury PSF still looks undervalued. This isn’t just prestige—it’s a value gap waiting to close.

- If you’re Singaporean → Look at OCR. At $1,950 psf, mass-market condos aren’t “cheap” anymore. Upgrading into CCR at $2,850 psf isn’t just indulgence—it’s smarter capital placement. You’re locking in prime at a relative discount.

- If you’re building legacy wealth → Freehold CCR homes are more than just assets; they’re heirlooms. You’re not just passing down bricks—you’re passing down status, address, and permanence.

Here’s how I put it to my clients:

“The worst time to buy CCR is when it’s already roaring. The best time is right before the roar.”

And based on this 3.0% surge, I’d say—we’re hearing the first growl.

A Few Hotspots Worth Watching

Orchard Boulevard / Tanglin – Ultra-prime is alive and kicking. Take 21 Anderson—a freehold project that’s quietly pulling buyers who still believe in the power of Orchard prestige. Even in a cautious climate, these deals don’t sit long.

Marina Bay / Shenton Way – Forget the “office-only” tag. With Skywaters Residences and a string of mixed-use luxury projects, this stretch of the CBD is morphing into a live-work-play district that feels closer to Hong Kong’s Central than old Singapore. Investors who missed the first Marina Bay wave don’t want to miss this second one.

River Valley / Robertson Quay – Perennial expat favorite. Freehold stock here is finite, rental demand is resilient, and the cosmopolitan riverside lifestyle keeps this pocket attractive whether the market is hot or cold.

Why CCR Always Bounces Back

Did you know what's the part most people overlook? CCR is capped.

New condos can keep sprouting in the OCR and RCR, but Orchard, Marina Bay, Newton? Supply is at the mercy of government land release and the rare en-bloc. That scarcity acts like a spring—it compresses in slower years, then releases in powerful upswings.

If you flip back through Singapore’s property cycles, the pattern is unmistakable:

- CCR drifts sideways while suburbs surge.

- Buyers start chasing “value” in OCR and RCR.

- Then, almost like clockwork, CCR snaps back—often outperforming everything else.

And right now, 2025 feels like the early innings of that snapback.

Where Do You Stand as an Investor?

Here’s my personal take.

If you’re waiting for CCR to “prove itself” further, you’ll probably end up chasing the market higher. This quarter’s 3.0% growth is exactly the kind of early signal we usually look back on and say, “That was the bottom.”

The long-term upside is still intact. CCR is the last piece of the puzzle that hasn’t run ahead. If OCR and RCR are already stretched, the smart money rotates back into prime. And when that shift happens in full swing, prices don’t creep up — they sprint.

Imagine it’s 2027. CCR has climbed another 20–25%. You’re sitting across from me again, and you’re telling me,

“Josh, I should’ve listened. I thought I had time. I didn’t.”

That’s the regret I don’t want you to have.

Today, you still have the advantage of choice.

- Units are available.

- Sellers are negotiable.

- Developers are realistic.

But give it another 12–18 months? The narrative will shift and that’s when the crowd rushes in.

This is Your Window.

If you’re serious about diversifying your portfolio, or if you’ve always wanted a foothold in Singapore’s most prestigious districts, don’t sit this one out.

Message us now!